Beyond the Hype: 5 Surprising Realities of the 2026 Art Market

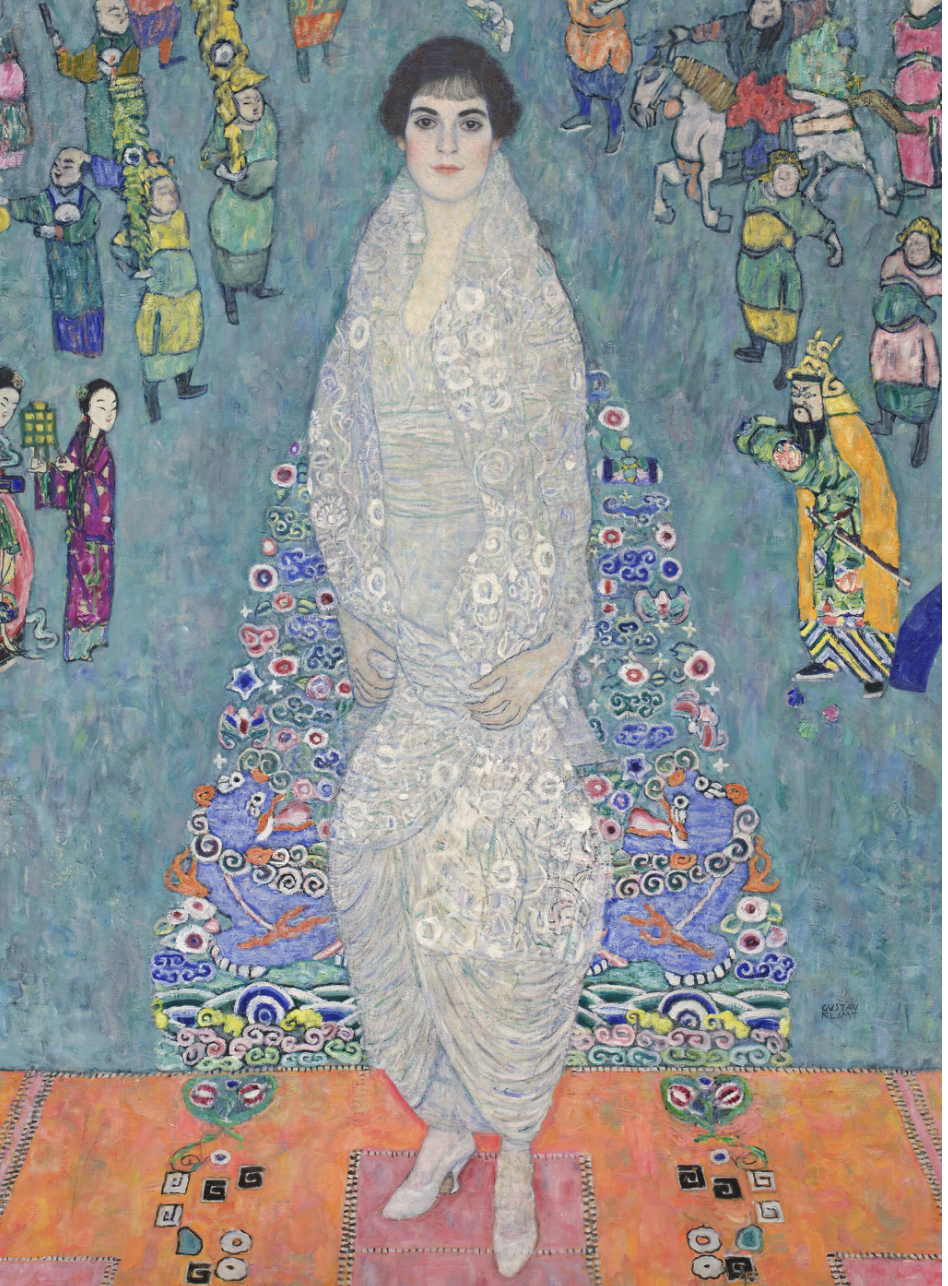

Gustav Klimt, Bildnis Elisabeth Lederer (Portrait of Elisabeth Lederer), 1914-1916. Sold for $236,360,000 USD at Sotheby’s New York on 18 November 2025.

Introduction: The End of the "Wild West" Era

The feverish, post-pandemic volatility that defined the early 2020s has finally broken, giving way to a period market leaders describe as the "Return to Discipline." While global art sales reached a resilient $59.6 billion in 2025—successfully reversing years of contraction—the underlying mechanics of the trade have fundamentally matured. We have exited the "Wild West" era of frantic digital speculation and overnight sensations. In its place is a market defined by intentionality, where the momentum has shifted decisively from high-frequency flipping to institutional-grade, long-term ownership.

This recalibration suggests a healthier, more grounded ecosystem. While total volumes remain below the speculative peaks of 2022, the current demand is anchored by a "Flight to Quality." As we navigate the 2026 landscape, five surprising realities reveal how collectors are prioritizing value, provenance, and price certainty over the transient "hype" of previous cycles.

Here are five takeaways based on findings from The Art Basel and UBS Global Art Market Report 2026 and Bank of America 2026 U.S. Art Market Report. Artamour Advisory’s comprehensive 2026 Art Market briefing report for collectors can be accessed here and below.

1. The Death of the "Flip": Why Patience is the New Alpha

For the short-term speculator, the current market is a minefield. The latest data on holding times delivers a definitive blow to the "flipping" culture that surged during the 2021–2022 NFT and Young Contemporary craze. Works held for under five years—the typical window for speculative resale—underperformed significantly, yielding an average loss of -5.7%.

Conversely, the market is aggressively rewarding the patient collector. Premium assets held for 20 years or more delivered a commanding +11.0% annualized return. This disparity marks the market’s divorce from the speculative era; today’s alpha is found in the "long cycle," where art is treated as a generational hedge rather than a liquid commodity.

"What we saw in 2025 was not a return to speculation, but a return to discipline. Major collections and estates came to market, which enabled collectors to focus on quality, provenance, and long-term significance."

— Drew Watson, Managing Director, Head of Art Services at Bank of America

The entrance of these "blue-chip" inventories—specifically landmark estates like those of S.I. Newhouse and Leonard A. Lauder—has anchored the market, forcing collectors to measure their acquisitions against historically significant benchmarks rather than social media trends.

2. Why Women Artists are Outperforming the Market

The most significant structural shift of the decade is the "Gender Alpha." This is no longer merely a cultural trend; it is a profound market correction. For decades, works by female artists were systemically undervalued, creating a massive valuation gap that is now closing with velocity. Over the last ten years, cumulative public auction sales for women rose by 105%, while their male counterparts saw a 37% decline from their 2015 peaks.

The financial incentive for this realignment is undeniable. In 2025, works by female artists delivered 15% annualized returns, outperforming the returns on male artists (4.7%) by a factor of three. This performance is bolstered by a primary market that has finally reached "perfect parity," with leading galleries now maintaining 50% female representation on their rosters. For the strategist, the message is clear: the highest potential for appreciation currently lies in this historical correction.

3. The Great U.S. Migration: California and the "Big 4" Concentration

The geography of American wealth is being redrawn, and the art market is following the money. While New York remains the undisputed capital—claiming a dominant 69% share of global auction totals—the broader Northeast is losing its absolute grip on the $1 million-plus market. That share has plummeted from 53% in 2015 to just 32% in 2025.

In its place, we see a "West Coast Ascendancy" and a tightening concentration of liquidity:

The California Surge: The West Coast now leads the U.S. with 35% of total transactions and a formidable 31% of the $1 million-plus market.

The "Big 4" Dominance: A staggering 81% of all $1 million-plus transactions are now concentrated in just four states: California, Florida, New York, and Texas.

The Sunbelt Influence: The migration of high-net-worth individuals to Florida and Texas has turned the Southeast and Central South into vital liquidity hubs, decentralizing the traditional New York-centric model.

4. The "Guaranteed" Gilded Age: Safety Over Scarcity

The U.S. auction market’s 23% rebound to $3.17 billion can largely be attributed to sophisticated risk mitigation. In a quest for price certainty, auction houses and consignors turned to guarantees (both internal and third-party) at an unprecedented scale. Guarantees reached a historic high of 78% of the total value of evening sales.

This creates a fascinating paradox: extreme risk aversion is actually driving record-breaking prices. These guarantees act as a psychological floor, removing the "failure to sell" risk and emboldening bidders to compete for trophy assets. This strategy has proven remarkably effective, with guaranteed lots outperforming their pre-sale estimates by an average of 10.6%. In 2026, "price certainty" has become a more valuable commodity than scarcity itself.

5. The Modern Rebound vs. The "Young Contemporary" Correction

A rigorous "Flight to Quality" has split the market. High-value transactions are migrating strictly toward historical segments with proven provenance, while speculative "new" talent faces a severe repricing. The landmark estates such as Leonard A. Lauder and S.I. Newhouse acted as primary liquidity magnets in 2025-2026, drawing capital away from unproven names and toward trophy valuations.

Modern Art: Experienced an exceptional surge, with auction sales up +149% year-on-year, driven by a desire for defensive, "blue-chip" inventory.

Impressionist Art: Showed strong expansion, with global value across both dealers and auctions increasing by +11%.

Contemporary Dealers: Performance remained stagnant, representing 43% of total lots as the market adjusted to more realistic asset evaluations.

Young Contemporary: This segment is undergoing a "severe repricing." While volume remains healthy for works under $50,000, the top-end speculative valuations of previous years have collapsed, leading to the lowest performance relative to estimates across all segments.

Conclusion: Navigating the "Valuation-Based" Future

The 2026 art market is defined by a singular, overarching theme: Value Over Speculation. From the rewarding of long-term holding times to the surge in guaranteed evening sales, the data points to a buyer who prizes certainty and historical significance over momentum.

As you evaluate your own holdings, the essential question is no longer about the "next big thing," but about structural integrity. For the blue-chip investment collector, is your portfolio positioned for the long cycle, or is it still carrying the baggage of the speculative era?

At Artamour Advisory, led by Principal & Founder Kristen de Bruyn, we help collectors navigate this disciplined new ecosystem. We align aesthetic passion with a rigorous, valuation-based lens, ensuring that every acquisition is not just emotionally resonant, but backed by the clarity of market data.

Source: The Art Basel & UBS Art Market Report 2026; Bank of America 2026 U.S. Art Market Report